- Introduction. Who Are CZ and SBF?

- How Did It All Start? CoinDesk Investigation

- The War Begins

- Shit Hits the Fan

- Bury the Hatchet? Or…

- Sam Bankman-Fried. From a Billionaire to Millionaires

- What Does This War Mean for the Crypto Market? The Bubble We Deserved

- SBF’s Bill and Political Conspiracies

- Conclusion. What Awaits the Crypto Market Next

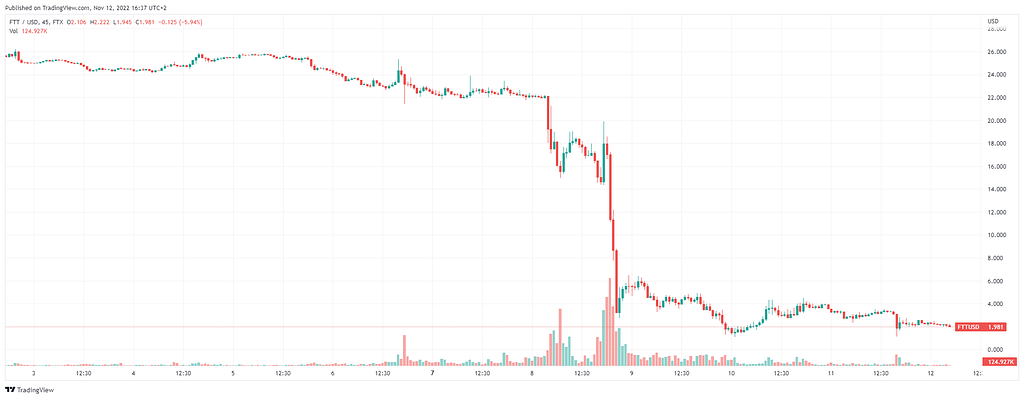

Crypto enthusiasts will remember the evening of November 8 for a long time. Blood was shed in the markets. The BTC price briefly dropped to $17,419.71, altcoins lost about 10-15% of their value, while the FTT token, the real culprit, crashed by 73%.

You are about to get answers to the most pressing questions at the moment: what happened to the market, why it dropped so much, and what the liquidity crisis is. We will also analyze the timeline of events of November 8 and speculate whether this is the end and what awaits the crypto industry next. It is a fascinating story of the struggle between two powerful crypto billionaires that has set the crypto market back a few steps, pointed out its weaknesses, and pulled out curious skeletons from the closets of the pillars of the industry.

Introduction. Who Are CZ and SBF?

Let’s start our story by introducing its protagonists. They are two pillars of the crypto industry. Two people who helped to develop it a lot and two deadly rivals.

Changpeng Zhao, or, as he is commonly referred to in the crypto community, CZ, the founder and CEO of one of the largest crypto exchanges Binance.

In 2017, crypto exchanges were not so user-friendly. The interfaces, as Zhao himself said, were “clunky,” the systems were slow, and there was no customer support. CZ literally revolutionized the industry by bringing a user-friendly product to the market. Binance turned the market upside down and took the lead among all platforms.

In early 2021, CZ first made it to the Forbes list with a net worth of $1.1 to $2 billion. However, according to the reputable Chinese magazine China Caijing, which considered his 30% stake in Binance, CZ had a fortune of $90 billion. And that is not a final figure either. People close to Zhao claim that he owns 90% of Binance.

Sam Bankman-Fried. The guy whose ugly business is the primary reason why you can read this article today. He is the founder and CEO of the FTX crypto exchange and the Alameda Research fund. In early 2022, Forbes estimated his fortune at $16.6 billion.

And to give you an idea of how influential this young man used to be, just look at the portfolio of his fund, which was often called the shadow force of the crypto market:

These two have not always been rivals. When FTX just launched, the head of Binance became one of its first big investors. But then, the two richest crypto billionaires parted their ways, with Bankman-Fried buying back Binance’s stake in FTX in 2020.

In one of his older tweets, Sam Bankman-Fried hinted that he was lobbying interests in Washington. The head of Binance is not allowed to these offices, which further fueled the feud between CZ and SBF. What interests and which bill Sam lobbied so actively will be revealed at the end of this article.

How Did It All Start? CoinDesk Investigation

Two crypto billionaires were living in peace, making money on newbie traders, manipulating token prices, increasing their fortunes, and only occasionally messing with each other.

But on November 2, CoinDesk published an investigation that immediately went viral on crypto media. The investigation focused on FTX and Alameda Research. These are two sister companies, as Sam Bankman-Fried owns 50% of FTX and 100% of Alameda. Reporters gained access to the latter firm’s internal documents and discovered large amounts of FTT tokens on Alameda’s balance sheet. FTT is a utility token of the FTX exchange that can be used to trade and conduct financial transactions.

According to the investigation, as of June 30, Alameda Research had $14.6 billion in assets, including $3.66 billion in “unlocked FTT” and $2.16 billion in “FTT collateral.” These were the company’s largest and third-largest assets, respectively. Experts have concluded that most of Alameda Research’s net worth was its own centrally controlled token. What does that imply? Well, imagine that SBF created his own token, inflated its price to the sky, and then scored loans for his second company using the token as collateral.

An important thing is that such a huge amount of FTT tokens (more than $5.8 billion) is highly illiquid: at the time of CoinDesk publication, only $5 billion of these tokens were in circulation. It means that an attempt to sell such a large package of FTT tokens would have led to a sharp drop in their price and, most likely, to the bankruptcy of Alameda itself. What’s more, Lucas Nuzzi, the head of research at Coin Metrics, identified from the open blockchain data that FTX had provided $4 billion in emergency funding to Alameda with FTT tokens. So, if Alameda goes bankrupt, the repayment of loans issued by FTX will come into serious question.

1/ I found evidence that FTX might have provided a massive bailout for Alameda in Q2 which now came back to haunt them.

40 days ago, 173 million FTT tokens worth over 4B USD became active on-chain.

A rabbit hole appeared 🧵👇 pic.twitter.com/DtCyPspME0

— Lucas Nuzzi (@LucasNuzzi) November 8, 2022

The War Begins

Negative news around Alameda and FTX emerged right away. The CEO of Bybit accused Sam Bankman-Fried of breaking his promise by selling 100 million BIT tokens, despite the agreement to hold them for at least three years. The BitDAO exchange community initiated a vote: Sam had to prove that no BIT tokens had been sold, or the community would consider ways to get rid of 3.36 million FTT on their balance.

Following the release of the investigation, the head of Binance posted a thread on Twitter where he revealed that his company had received $2.1B in BUSD and FTT as part of their exit strategy from FTX investments. He also noted that, due to SBF’s unethical behavior, they were going to sell a $600M stake in FTT tokens within 1-2 months in the open market.

As part of Binance’s exit from FTX equity last year, Binance received roughly $2.1 billion USD equivalent in cash (BUSD and FTT). Due to recent revelations that have came to light, we have decided to liquidate any remaining FTT on our books. 1/4

— CZ 🔶 Binance (@cz_binance) November 6, 2022

CZ planned to crash FTT and cause a liquidity crisis for FTX and Alameda. Alameda Research CEO Carolyn Ellison publicly urged CZ to sell all FTT tokens at $22 to reduce the market impact, but CZ refused the offer, saying it was a free market.

FTX clients encountered the first withdrawal issues on the morning of November 7. FTX responded to reports by claiming that slow Bitcoin withdrawals were due to limited network bandwidth. SBF said FTX had no credit issues, and Carolyn Ellison added that Alameda had $10 billion in undisclosed funds, while most of their loans had been repaid.

Shit Hits the Fan

CZ’s plan worked. His announcement immediately led to a massive outflow of funds from the exchange. According to Nansen:

- NEXO withdrew ETH worth $114M;

- The 0x1bf0 address withdrew USDC worth $79M;

- The 0x645c address withdrew ETH worth $31.7M;

- The Arca fund withdrew ETH worth $18M;

- And so on.

The largest users withdrew more than $419M in 24 hours, and that’s not considering all the others.

FTX, in turn, was trying to stay afloat, replenishing its wallets through Circle, the issuer of USDC. However, capital outflows sustained, and FTX’s hot wallets continued to go empty. To stem the outflow, FTX paused withdrawals (according to The Block citing data from blockchain explorers). Transactions from the main wallets on the Ethereum, Solana, and Tron networks were not carried out for about two hours. Curiously enough, right after the publication of The Block, withdrawals were brought back.

By the evening of November 8, the FTT token had lost more than 70% of its value.

Apparently, the exchange used its clients’ assets for questionable purposes, so it became unable to meet its obligations when everyone suddenly decided to withdraw their funds. In previous cases that involve big bankruptcies in the crypto world (Celsius, Voyager, etc.), projects used clients’ funds to invest in risky ideas, hoping to make more money. In FTX’s case, it seems to be about using clients’ funds to “save” Alameda, which belongs to the same owner.

The fall of the Terra/Luna crypto Ponzi scheme in May 2022 shattered many crypto funds, but Alameda was seemingly unaffected by the chaos unfolding in the market at the time. Now, it’s clear that this stability was only a fiction. In fact, the hole in Alameda’s balance was just hastily plugged with FTX funds.

Sam Bankman-Fried found himself in an extremely pitiful position and had to take a desperate step.

Bury the Hatchet? Or…

The same evening, SBF called CZ and proposed an ingenious deal. Yes, CZ’s ardent opponent saw no other way out. He asked his competitor for help and offered a strategic deal to take over his exchange:

Our teams are working on clearing out the withdrawal backlog as is. This will clear out liquidity crunches; all assets will be covered 1:1. This is one of the main reasons we’ve asked Binance to come in. It may take a bit to settle etc. — we apologize for that.

The head of Binance, in turn, stated:

This afternoon, FTX asked for our help. There is a significant liquidity crunch. To protect users, we signed a non-binding LOI, intending to fully acquire http://FTX.com and help cover the liquidity crunch. We will be conducting a full DD in the coming days.

However, after full due diligence on FTX and Alameda Research assets, Binance declared it was backing off from the original deal.

As noted by Matt Levine from Bloomberg, if one exchange asks another larger one for help and they reach an agreement within one day, it almost certainly means that the seller simply had no other choice, and the price of such a sale is likely to be close to a symbolic one dollar. Apparently, the size of the hole in FTX’s balance sheet is too big to justify Binance buying one of its biggest competitors. According to Bloomberg sources, during a recent investor call, Sam Bankman-Fried said that FTX may need an emergency capital injection of $4 to $8 billion to avoid bankruptcy.

As for the misuse of user funds, this is indicated by the fact that no one was able to identify FTX cold wallets. Most of Alameda’s transfers to FTX for stablecoin deposits were from hot wallets. The exchange’s desire to conceal information leads to the conclusion that farming by Alameda from the very beginning of the exchange had been funded with users’ assets.

As might be expected, after Binance announced its withdrawal from the deal, the market continued to fall.

Sam Bankman-Fried. From a Billionaire to Millionaires

How could a man whose companies were called the shadow force of the market and who half of the crypto community prayed to, lose his empire in a few days?

The answer is simple. He overplayed his hand. Not only did he create a bubble of an unprecedented scale (much bigger than Terra/Luna), but also invested his FTX exchange clients’ money through Alameda. As practice shows, if you commit fraud, you will never win at a distance.

SBF’s fortune went down from $16.6 billion to $991.5 million in two days.

What Does This War Mean for the Crypto Market? The Bubble We Deserved

The current showdown between the owners of major crypto exchanges comes amid a bear market and looming heavy regulation from the US. This is a serious blow to the industry. People trusted SBF, but it was a big mistake. Unlike the Terra/Luna bankruptcy, Alameda Research and FTX were active investors in countless leading blockchain projects. SBF’s hands are elbow-deep in altcoins (for example, FTX owns 10% of SOL tokens). If FTX is unable to meet its liabilities, they will start selling off all the assets, and there are a lot of them.

Solana already had its own problems, and now all the projects based on it are in the same situation as SBF himself. Just six months ago, everyone would have been calm, but the collapse of Terra/Luna has shown how a large-scale blockchain can go down in just a few days.

The OKX crypto exchange founder urged CZ to make a new deal with Sam Bankman-Fried and refrain from selling FTT:

If, unfortunately, FTX becomes another LUNA, nobody in the industry can benefit from the accident, including Binance. Both customers and regulators will lose some confidence about the whole industry.

But the head of Binance is unlikely to listen to him and take any steps to save FTX, especially given the SEC’s recent announcement about an investigation into the FTT token they are starting with the US Department of Justice.

SBF’s Bill and Political Conspiracies

SBF has spent millions on lobbying for his project and political donations. Moreover, he used to be the most vocal industry representative in Washington. Minutes after the FTX exchange boss made the shocking decision to sell his business to Binance on Election Day, industry insiders said that his priority bill was effectively “dead.”

The FTX head was taking a proactive regulatory stance, attempting to significantly limit the rights and freedoms of DeFi protocol creators. Among other things, this implied protocol front-end licensing, so that the US and other jurisdictions with strict legislation could not use DeFi infrastructure, and the winning side, of course, would have been centralized exchanges, including, first and foremost, FTX.

The bill and Sam Bankman-Fried himself were heavily criticized by supporters of decentralized finance, who said the legislation would hurt their projects. Once the revised version of the bill became public, the criticism reached a frenzy, resulting in the private objections of technology advocates being heard “at the top.”

And since SBF donated a lot of money to the Democratic Party, rumors were flying that the CoinDesk investigation came out just before the elections for a reason.

Conclusion. What Awaits the Crypto Market Next

Undoubtedly, the market needs time to recover. Moreover, we don’t know the ultimate consequences yet as the situation is still developing.

This year has been especially rich for all sorts of weird stuff in the crypto world: we have already seen epic collapses of Terra/Luna, Celsius, and Three Arrows Capital. Each event of this kind spreads in waves and induces all crypto assets to fall due to a market-wide panic. Don’t expect this time to be different. The transformation of FTX, the fourth-largest crypto exchange by trading volume, into a full-fledged bankrupt in just a few days came as a shock to crypto investors.

On November 8-9, Bitcoin fell by more than 20%, while Ether lost almost 30% of its value. The price of Bitcoin briefly dipped below the $16 000 mark, which wasn’t seen since November 2020. So-called “altcoins” also suffered major losses. For example, Solana (SOL), which was another of Alameda’s major positions, depreciated by more than a half in two days.

In response to user concerns, a number of major crypto exchanges, including Huobi, OKX, and KuCoin, have announced their intention to begin publishing “transparent” reports on their reserves directly on the blockchain. Binance has already done so by posting a list of crypto addresses with assets totaling $69 billion.

As part of #Binance‘s ongoing commitment to transparency, we are sharing details of our hot and cold wallet addresses.

Stay tuned as we will publish a Merkle tree proof of funds within the next few weeks.

More details here ⤵️

— Binance (@binance) November 10, 2022

With all the things happening now in the world of crypto, we should expect that the aftermath of FTX’s collapse will continue to come in waves in the future. After all, we don’t know the full scale of the problem yet. What other big players kept liabilities of FTX and Alameda as their assets on balance sheets? Do they have free capital to plug the holes? A series of high-profile bankruptcies may continue, causing the crypto market to drop even further.

The developments in the blockchain world are starting to look a lot like the financial crash of 2008. Back then, the scariest words for financiers were “financial contagion.” Everyone feared that the problems of big players (Lehman Brothers, Bear Stearns) would cause a domino effect for their counterparties, which would eventually destabilize the entire financial system.

Specifically, BlockFi, a crypto trading company, froze withdrawals on November 11. Presumably, nearly $4 billion in BlockFi customer funds were stored on the ill-fated FTX. A few months ago, Sam Bankman-Fried bailed out the then-bankrupt BlockFi by giving them out a $400 million loan. At the time, it could be written off as altruism and a desire to prevent the collapse of the crypto financial system as a whole. But in light of recent events, Sam’s goals look somewhat different.

You put $400 million of your own money to save BlockFi and then ask them to store $4 billion of customer assets on your exchange which, in turn, can be poured into the sinking fund. Although this is purely a speculative view, it is impossible to estimate how many more of these companies left their assets with FTX or Alameda. Therefore, we should be fully prepared for new surprises of this kind in the near future.

As Changpeng Zhao noted in an internal memo to his employees, these events have “severely shaken” confidence in the crypto industry, so it’s not a victory for Binance either.

“Regulators will scrutinize exchanges even more. Licenses around the globe will be harder to get. People now think we are the biggest and will attack us more,” he wrote.

On Friday, November 11, FTX officially filed for bankruptcy under the so-called Chapter 11. This means that the company will continue to operate while the newly appointed managers are trying to come up with a rescue plan. For the exchange’s clients, this can hardly be good news. If they manage to get some money back, it may happen only in a few years and only partially. The paperwork filled out by the exchange shows that as many as 130 companies are included in the bankruptcy proceedings. This includes Alameda, the international division FTX.com, and the regulated entity FTX.US. Concurrently, Sam stepped down as FTX CEO.

On Saturday night, over $600 million was transferred from FTX wallets. The official FTX Telegram support channel claims it was a hack. Things are moving rapidly, and while FTX may already be dead, there are likely many more unexpected twists in this story to come. We will keep monitoring the developments and keep you updated.